Home > Politics

As the use of independent cryptoassets by small and medium-sized European companies with high international exposure grows[1]The European Parliament's Committee on Economic and Monetary Affairs (ECON) voted on the MiCA Regulation (Markets in Crypto-Assets) on 10 October 2022. The main objective of this project is to establish a common framework for all European Union (EU) Member States that have developed their own regulations on cryptoassets. Germany, Lithuania, Malta and France are the most advanced. Considering in particular the increase in the number of cryptocurrency-related cyber attacks from "2.9 % of all reported cyber threats in [January] 2021, [to] 8.4 % from February to October 2021"[2]The European institutions intend to introduce a regulatory framework for consumer protection applicable to platforms in case of loss or piracy of investors' assets.

This is without taking into account the European will to mitigate the risks of money laundering and terrorist financing, which may be permitted by the non-traceability of transactions carried out within the framework of decentralised finance not backed by central banks. The EU Member States remain aligned with Recommendations 15 and 16 of the Financial Action Task Force (FATF), for example with regard to the 'Travel Rule'. on transparency as to the origin and beneficiary of cryptoassets. There is therefore no major difference between the EU text and the FATF on the key points of compliance. Similarly, service providers whose headquarters are based in the territory of a third state considered "to be high risk in terms of anti-money laundering activities as well as on the EU list of non-cooperative countries and territories for tax purposes will be required to implement enhanced controls in accordance with the EU framework"[3].

Between regulatory requirements, controls and the promotion of an innovative investment technology, the future MiCA regulation is not without controversy on the potential encouragement or hindrance to the use of the solution that cryptoassets represent for businesses. On the one hand, cryptoasset sales and exchange platforms are expressing some fears about the development of a regulatory framework that is too far removed from the business reality and positioning of other jurisdictions, particularly in Africa. On the other hand, on the other hand, the world of banking compliance is calling for strict control by European decision-making bodies. The provisional agreement reached by the Council of the European Union and the European Parliament on 30 June 2022 was a balance between the different visions. However, the leakage of an updated version of the compromise text in September 2022 suggested that the draft contained new provisions that could hamper the adoption of independent cryptocurrencies by European businesses. The finally adopted, substantially different draft is not expected to come into force before the end of 2024. It already outlines a political vision of the arbitration between two visions of finance and the prospects of appropriation of this new tool by companies.

Indeed, independent cryptocurrencies can be considered by companies as an alternative solution to the difficulty posed by the over-compliance of banking institutions, which prefer to refuse to operate, as a precaution, transactions that are nevertheless authorised in view of the complexity of the nexus and the potential conflict between the European and cross-Atlantic sanctions regimes. Now a company can buy so-called cryptocurrencies stablecoinsFor example, a company that stores x grams of gold or x dollars per cryptocurrency to avoid volatility, and sends it to the recipient without going through a bank. While compliance issues remain in decentralised finance, the over-compliance of banks disappears. The initial cost of these checks is then amortised by the savings in bank fees. Transactions become near-instantaneous whereas several weeks would be required with one of the few banks that would agree to proceed with the transaction. The use of cryptocurrencies then offers access to new and promising markets.

However, the benefits of using independent cryptocurrencies could be limited by these new provisions of the MicA regulation. As it stands, the integration of tokens non-fungible (NFT) and stablecoins The most problematic issues are the algorithmic measures and the question of unfair competition from foreign platforms not subject to MiCA. These measures particularly affect European platforms, which process payments and trade for businesses. Platforms are now required to increase their compliance, with costs and delays being passed on. This will discourage businesses that use a platform on an ad hoc basis, as the competitive advantage of these platforms over banks is no longer as attractive. Others, which have a continuous and significant need, will continue to use them or carry out these transactions directly, without platforms, even if it means investing and training their teams. Finally, it is a compromise solution, as some economic players may use non-European platforms, which is not prohibited as long as there is no active solicitation.

The problem is therefore deeper, the growing difference between the EU's restrictive regulation and that of other more accommodating jurisdictions. The very choice of proceeding by exhaustive regulation, where the United States wants to regulate by progressive judicial decisions, does not allow the flexibility necessary for an innovative sector. The question then arises as to the issues underlying this choice. The European Union, unlike Washington, is planning to set up a central bank digital currency, the e-euro, which is a competitor for independent cryptocurrencies and stablecoins ... some of these should be regulated by MiCA.

All rights reserved by BRAUN

An untraceable digital tool for business development, cryptoassets are an innovative technology that allows companies using them to reduce banking fees and delays for their transactions. In the face of increasing regulation by governments and the European Union[1]and their appropriation by banks, this instrument could move from challenger à MaverickThis is a non-conformist trend.

European companies, especially small and medium-sized enterprises (SMEs) and French mid-sized companies (MSEs), have been strongly encouraged by their governments to expand their exports in search of the liquidity they could no longer easily find since the crisis generated by the anti-COVID measures[2]. In doing so, they have had to deal with a variety of banking difficulties: fees considered excessive, delays inappropriate and over-compliance. For example, a French company that imports cocoa for processing is often confronted with bank charges that are considered high for a transfer to Côte d'Ivoire. These are explained by a structural part linked to the costs of the bank but also to the local network. The said transfer will not take place without longer delays and without an increase in documentary requests. As a result, the cost of the raw product cuts into the margin and the delays disrupt production. The traditional banking channel then becomes a significant brake. This trend is particularly noticeable in demanding markets such as the authorised sectors of countries under sanctions or so-called "frontier" markets, i.e. markets with a high commercial potential but which do not yet provide sufficient liquidity and reliable financial networks.

The use of cryptoassets by businesses for these transactions is growing, with "Europe [being] the largest crypto-economy in the world, receiving some $1 trillion in crypto-currencies [in 2020], representing 25% of global activity. The US is the second largest region, with $750 billion in value received, or 18%."[3]. A crypto asset is a cryptographically generated digital asset issued peer-to-peer through a decentralised computer network. Credit balance verification, clearing and bookkeeping are performed by a multitude of decentralised trusted third parties, which are computers. Confirmation from all of them is required to validate the transaction. One of these third parties receives financial compensation at random.

The use of cryptoassets is proving to be almost instantaneous, more secure and, above all, much cheaper from a business perspective. Solutions are emerging to maintain these advantages in compliance with stablecoins regulated and promoted by the United States as well as with cryptoassets backed by the Chinese Central Bank. The volatility risk is offset by these stablecoinsThe European regulation announced (MiCA) seems to be restrictive despite the fact that it allows for traceability of digital assets. The announced European regulation (MiCA) seems restrictive despite the traceability provided by the BlockchainThe underlying technology of cryptoassets. Banks and other platforms are therefore rushing to integrate these products into their offer, promising to guarantee the compliance of operations with the PSAN registration of the Autorité des Marchés Financiers. The result is a MaverickThis is a real innovation but far from what was initially hoped for.

It is at this point in the evolution of the banking and financial market that cryptoassets take on a decisive geopolitical dimension. Cryptoassets, whether independent or issued by a central bank, challenge both the hegemony of the dollar and the effectiveness of US sanctions. On the one hand, they offer an alternative as a store of value, since most of these currencies cannot be printed,[4] and means of exchange, as they are decentralised and therefore not very permeable to political pressure. On the other hand, these currencies prevent the information feedback that would allow the United States to sanction easily. Washington therefore promotes the use of stablecoins dollar-backed and classified as securities and therefore framed by the Security and Exchange Commission (SEC). This would considerably strengthen the position of the dollar. China, notably through the Regional Comprehensive Economic Partnership, the largest free trade agreement in the world[5]In addition, the European Commission is gradually promoting the use of local currencies and, above all, central bank cryptoassets, which are capable of challenging the dollar's position while retaining state control and connection to the banking system.

The European Union, meanwhile, has been dithering over the desirability of an e-euro but seems to have taken the side of strict regulation of independent cryptoassets, at the risk of weakening their usefulness. Other jurisdictions, notably in Africa, have made considerable progress towards these central bank currencies[6]. Cryptocurrencies represent only a part of the cryptoassets that can facilitate transactions for French companies (NFT in particular). These, together with innovative instruments such as smart contractsThe potential is great for European businesses internationally. The potential is great for European companies internationally... if future regulation agrees to take this into account.

All rights reserved by BRAUN

Taipei, Taiwan, 2-3 August 2022. A surprise visit by the Speaker of the US House of Representatives Nancy Pelosi took place and the news reverberated across the Asia-Pacific[1]. Beijing reacted sharply by deploying ships and aircraft around Taiwan on 4 August as "large-scale aero-naval exercises", including ballistic missile launches[2]. Numerous Chinese military drones (BZK-007) have entered the island's Air Defence Identification Zone (ADIZ)[3]. Several Chinese aircraft have crossed the median line of the Taiwan Strait[4]. On 20 August alone, the Taiwanese Ministry of Defence reported 17 warplanes and 5 Chinese army vessels in the vicinity of the island[5]. Also, according to the ministry, seven of the 17 aircraft (two Xi'an JH-7 bombers, two Sukhoi-30s, two Shenyang J-11s and a Shaanxi Y-8 anti-submarine aircraft) crossed the median line separating China and Taiwan in the Strait, or ventured into the southwestern sector of Taiwan's Air Defence Identification Zone (ADZ)[6]. According to a database compiled by AFP from Taiwanese military reports, there were some 446 air incursions by Chinese warplanes into Taiwan in August, and 1,100 since the beginning of the year[7].

However, these Chinese reactions are nothing new. Since the advent of the People's Republic of China and the exile of Chiang Kai-Shek to Taiwan in 1949, the question of the island has been a bone of contention between Beijing and Taipei.[8]. The former considers Taiwan as its province, while the Taiwanese want to keep their independence, in opposition to the "one China principle" (One China principle)[9].

Second, although Western countries (with the exception of the Vatican) no longer have embassies in Taipei, they have maintained and increased their contacts with Taiwanese officials[10].

As early as 1979, despite Washington's recognition of China, the United States ratified the Taiwan Relations Act (TRA), through which they committed to supply Taiwan with sufficient arms to enable it to defend itself in the event of military aggression[11]and this commitment still exists today[12]. President Ronald Reagan's Six Assurances (1982) also characterise the US commitment to Taiwan[13]. They are: (1) not to set a date for the cessation of arms deliveries to Taiwan; (2) not to consult Beijing on arms sales to Taiwan; (3) not to mediate between Taipei and Beijing; (4) not to revise the terms of the TRA; (5) not to change its position on the issue of Taiwan's sovereignty; and finally, (6) not to put pressure on Taipei to open negotiations with Beijing[14].

On 2 September, the US government authorised three new arms sales to Taiwan totalling US$1.1 billion, which include logistical support for the radar surveillance programme and related equipment, including 60 AGM-84L-1 Harpoon Block II missiles, and 100 AIM-9X Sidewinder Block II missiles[15]. According to the Taiwanese Foreign Ministry, this is the fifth announcement of arms sales to Taiwan by the Biden administration this year, and the sixth since the US president's inauguration in January 2021[16].

In addition to Pelosi and other US lawmakers[17]Japanese officials[18]and some European representatives (Lithuanian, Czech and Slovak) have also made recent visits to Taipei[19]As was the case for the French recently (7-8 September)[20]. Canadians prepare for October 2022 for a future parliamentary visit[21]. Beijing takes a dim view of these deepening relations[22].

Indeed, in addition to the South China Sea (Paracels and Spratlys), Beijing claims several islands along its eastern coast: apart from Taiwan, these include the Japanese islands of Senkaku[23]. This causes concern in Tokyo and even in Washington, because of its military bases in the region (Okinawa in Japan)[24].

However, Taiwan is the object of covetousness for both Beijing and Washington, not only because of its strategic location (Taiwan Strait), but also because of its industrial potential (ultra hi-tech factories) and its technological heritage (production of semiconductors)[25].

Taiwan's semiconductor industry, which is essential for the manufacture of high-tech products (telephones, aircraft, solar panels, etc.) and crucial to the world economy, accounts for a large proportion of world production (63 %)[26]. Taiwanese factories are capable of engraving large-scale chips with a precision of 3 nanometres (3 millionths of a millimetre), which are sold worldwide and equip our cars, trains, planes, refrigerators, telephones (90% of the latest generations of smartphones, all brands included).[27] Whether Asian, European or American, the biggest brands have become ultra-dependent on these Taiwanese semiconductors[28]. The most advanced semiconductors are largely manufactured by the Taiwan Semiconductor Manufacturing Company (TSMC) (the world's largest semiconductor company)[29].

Foxconn, one of Taiwan's largest technology companies, is Apple's main electronics supplier and assembles its iPhone[30]. Also China's largest private employer, Foxconn is under pressure from Taiwanese authorities to abandon an $800 million investment in Chinese chipmaker Tsinghua Unigroup[31]. Behind this pressure is a fear on the part of the authorities that a strengthened Chinese company will help China achieve its technological ambitions in its long-distance battle with the United States, especially as the Chinese investment company WiseRoad Capital, with close ties to the Beijing government, is named in the investment agreement alongside Foxconn[32]. Indeed, the United States is seeking to reduce its dependence on China, and in early August 2022, Joe Biden signed a bill entitled CHIPS and Science Act, which is releasing $52 billion in subsidies to boost semiconductor production in the US[33].

In addition to being a world leader in chip (or semiconductor) production, Taiwan also remains a strategic location that Beijing still seeks to control: the Taiwan Strait, 130 km wide between the People's Republic of China and the island of Taiwan, is also an important trade route between the South and East China Seas[34]The main reason for this is that it is used for cargo ships connecting China, Japan, South Korea and Taiwan with the West.[35]. According to data compiled by Bloomberg, nearly half of the world's container fleet, or 48 % of the world's 5,400 operational container ships, and 88% of the world's largest ships by tonnage passed through the Strait this year[36].

The island still has the advantage of direct access to the deep ocean on its eastern shores, which would allow China to build a new ballistic missile submarine (SSBN) base and move closer to the US coast[37].

Nevertheless, despite the threats of open war, economic and political actors are working to avoid an escalation for fear of paralysing the global economy[38]. However, to ensure security and stability of supply as well as to respond to Chinese influence, the Indo-Pacific Economic Framework initiative was launched during Biden's visit to Japan last May, and a summit involving 14 countries (in addition to the US and Japan, Australia, Brunei, Fiji, India, Indonesia, Malaysia, New Zealand, the Philippines, Singapore, South Korea, Thailand and Vietnam) began on 8 September in Los Angeles.[39].

Finally, the possible meeting of US President Joe Biden and Chinese President Xi Jinping at the G20 in Bali, Indonesia, in November 2022[40]This is the first time that the European Union has been involved in the development of the Taiwanese economy, which could shed more light on the fate of Taiwan, and indeed of the Asia-Pacific region, in the years to come...

All rights reserved by BRAUN

On the 25th of September Italians will go to the polls to elect a new Government after snap elections were called in the middle of summer. Political turmoil is not uncommon in Italy and even Mario Draghi was not able to survive the unstable Italian political scene.

The fall of Mario Draghi

Draghi was leading a national unity Government composed of basically every major party in Parliament except Giorgia Meloni's Fratelli d'Italia (ECR). The Premier lost its majority after a crisis started by the 5 Stars Movement (NI) leader Giuseppe Conte, following his threats of pulling out of the Government unless more 5 Stars policies would be included in the agenda. Thereafter, Mario Draghi had to address the Parliament regarding the ongoing crisis. His speech disappointed two other parties in the majority, Forza Italia (EPP) and Lega (ID), which had some complaints about certain passages of Draghi's speech. Lega and Forza Italia, then, proposed to continue with Draghi as a leader of Government but requested in exchange the assurance that the 5 Stars would not be included in the new majority. No agreement was found and as a result the government finally fell.

The players

Following the fall of Draghi, the parties scrambled to form alliances and coalitions for the upcoming elections. Two liberal parties (Azione and +Europa, Renew Europe) and socialists (PD + minor parties, S&D) were very close to find a deal to make a coalition in order to have a chance to challenge the centre-right bloc and even signed an official agreement to present a common coalition. Shortly after, the liberals from Azione, led by Carlo Calenda, broke off the coalition, while +Europa decided to stay. Following this split, Azione founded an alliance with Italia Viva (RE), the party led by the ex-Premier Matteo Renzi.

PD (S&D) later decided to include some minor far-left parties in its coalition, furtherly positioning itself on the left, making it easier for the liberal coalition to eat out its votes from the centre/moderates. PD presented voters with a programme centered on three 'pillars': Sustainable development and ecological and digital transitions; Jobs, knowledge, and social justice; Rights and citizenship.

One of the minor parties included in the socialist alliance is called "Sinistra Italiana", led by Nicola Fratoianni, known for its far-left positions on economic matters and skeptical views on NATO (opposed to the entrance of Finland and Sweden after the Russian invasion). The inclusion of Sinistra Italiana in the coalition led to criticism from all sides towards PD and its secretary Enrico Letta. Sinistra Italiana used to sit in the opposition seats during the Draghi Government.

Luigi di Maio, the outgoing Minister of Foreign Affairs, left the 5 stars movement earlier before the political crisis caused the fall of the Draghi Government, after some disagreements with Giuseppe Conte on the positioning of the party on the Russian-Ukrainian conflict. Tens of 5 Stars members of parliament followed Di Maio and left the movement. Di Maio, then, founded a political list called "Impegno Civico" which will be running together with the centre-left coalition led by PD.

In the meantime, Giuseppe Conte confirmed that the 5 stars movement will be running alone in the 2022 elections.

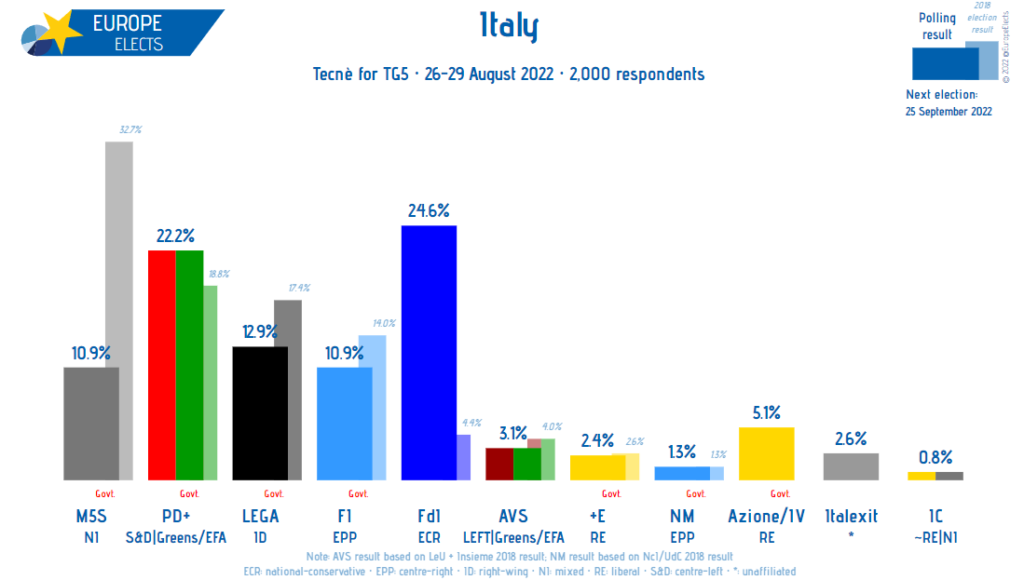

This is the best scenario for the centre-right coalition composed by Giorgia Meloni's Fratelli D'Italia, Matteo Salvini's Lega, Silvio Berlusconi's Forza Italia (EPP) and the centrist list Noi Moderati (EPP). The coalition is consistently polling around 48%, and with the current electoral law the center-right is projected to win a majority in both chambers, Camera and Senato. The centre-right coalition has an internal agreement regarding which party will be choosing the name to be proposed to the President to lead the Government. The party which will have the highest number of votes will be choosing the name. With today's percentages, Fratelli d'Italia should be the party nominating the future Premier and Giorgia Meloni is likely to be the candidate.

The favorites

This is the first chance in years for the centre-right to regain power after its last government, which was led by Silvio Berlusconi until its collapse in 2011. Eleven years later Berlusconi is ready for his comeback to Italian politics after his election as a Member of the European Parliament in 2019.

While Giorgia Meloni aims for the premiership, Matteo Salvini is focusing Lega's campaign on the security topic and his potential return as Minister of the Interior. Italy has been one of the main targets of illegal crossings and human traffickers through the Mediterranean sea and during this year's summer, the numbers of arrivals have once again skyrocketed and are reaching pre-covid numbers.

The centre-right coalition presented a common electoral programme, composed of 15 points. The initial point concerns the international positioning of Italy, defined as "fully part of Europe, the Atlantic Alliance and the West", and with the setting of a "foreign policy focused on the protection of the national interest and the defense of the homeland".

The document deals with various topics, including tax and justice reforms, passing through the review of certain welfare issues, the fight against illegal immigration, and environmental protection. The programme also includes a "revision of the PNRR (Recovery Plan) according to the changed conditions, needs and priorities" and the proposal of a reform of the Constitution, resulting in the direct election of the President of the Republic and the increase of regional autonomies.

The Outsiders

The liberal coalition formed by Calenda's Azione and Renzi's Italia Viva is polling around 5% (the threshold to enter Parliament is 3%) and has as its main target the moderate centrist electorate. Its programme is composed of progressive points and pragmatic views on energetic issues such as the necessity of the use of nuclear energy never used to this day in Italy.

On this point, the liberal coalition converges toward the center-right. The energy crisis is one

of the main topics being discussed during this election campaign which worries the most Italian voters. The high utility bills are already claiming victims among companies, the price increases will also weigh heavily on households. The center-left coalition and the 5 Stars are strongly against the use of nuclear energy, while the liberal coalition and the center-right are strongly in favor of its use and believe that any environmentally clean tool should be used to fight the energy crisis and move towards the energetic autonomy of Italy.

What to expect after the 25th of September

The center-right is projected to win, but what can we expect from the newborn Government? The conservatives will have to deal with one of the major crises in our recent history, the Russian-Ukrainian conflict, surging gas prices, and inflation. Furthermore, Brussels will be watching and will expect Italy to maintain the promises made during the Draghi Government. What will be the situation of Italian Government during one of the hardest winters in decades in Europe?

All rights reserved by BRAUN

Fourteen years have passed since the declaration of independence on 17 February 2008 in Pristina, Kosovo, and the situation in this part of the Western Balkans remains tense[1].

Belgrade refuses to recognise the independence of what it considers its southern province[2]. Several other European states, including EU and NATO states such as Spain, Slovakia, Romania and Greece, refuse to recognise Kosovo as an independent state[3]. Cyprus, Bosnia-Herzegovina, the three South Caucasus countries as well as Moldova, Ukraine, Belarus and Russia also refuse to recognise its independence[4]. This opposition still exists, and for several reasons such as the preservation of territorial integration and areas of influence[5].

Moreover, the declaration of independence took place in a context where Kosovo was ravaged by the war (1998-1999) between the Albanian separatists of the KLA and the Yugoslav authorities, as well as by the NATO bombing of Yugoslavia (March and June 1999[6]). These two events have left vivid memories among the Kosovar and Serb populations[7]. The United States and its European allies supported the Albanians, while Russia and China condemned the NATO bombing[8].

In spite of this, in order to resolve the Serbian-Kosovar conflict, the EU, like the USA, has organised numerous summits with Serbian and Kosovar representatives, which have still not led to a total easing of tensions[9]. Even the Brussels agreements in 2013, and the Washington agreements in 2020, have not led to the expected results of full normalisation[10].

Even today, many EU missions, such as EULEX Kosovo, and NATO missions, such as KFOR, remain in place in the country to ensure the stability and security of the Balkans[11].

By the end of July 2022, the Pristina government's border decisions on number plates and residence documents had led to protests among the Serb population in northern Kosovo[12]. The barricades set up by the Serbs at the time, blocking the border posts at these locations, had put NATO forces on alert[13]. Finally, it was following the intervention of the American ambassador, Jeffrey Honevier, that the Pristina decisions were postponed, allowing a return to calm[14].

All of this illustrates that the tensions between Serbia and Kosovo do not only concern Albanians and Serbs, but several powers (the United States, the European Union, Russia, China) that distribute their zones of influence in the Western Balkans[15].

With the exception of Croatia and Slovenia, the Western Balkan countries are not members of the European Union[16]Accession negotiations for Serbia and Kosovo slow down[17]. Moreover, the two states are, together with Bosnia-Herzegovina, the only ones in the Balkans that are not members of NATO[18]. However, Kosovo is home to the largest military base in the Transatlantic Alliance: Camp Bondsteel (3.86 km²), capable of hosting up to 7,000 troops[19]. The KFOR forces consist of more than 3770 troops from 28 countries[20]. However, NATO and Serbia have deepened their cooperation, including on security in Kosovo[21].

At the same time, Turkey and the Arab Gulf states, as well as Russia and China, have increased their economic and cultural, and even energy, investments in the Western Balkans (including Serbia and Kosovo)[22]. While the US and its allies support Pristina militarily (the case of the creation of the Kosovar army, disapproved by the Serbs)[23]Moscow and Beijing to deliver to Belgrade on armaments[24]. For example, in 2019, Serbia procured the Pantsir-S1 short-range surface-to-air system (20 km range) from Russia[25]. In 2020, Serbia obtained Chinese Chengu Pterodactyl-1 drones, "capable of attacking targets with bombs and performing reconnaissance tasks".[26]. Finally, in April 2022, six Chinese Air Force Y-20 aircraft carrying HQ-22 surface-to-air missiles landed in Belgrade[27].

Even in the energy field, Kosovo is strategically located, with several pipelines, such as the Transadriatic Pipeline (TAP) and the Balkan Stream, supplying gas to Europe, passing through the region and being the subject of rivalry between the European Union and Russia[28]. Brussels works to diversify its gas supplies while Moscow seeks to keep its export markets[29]. Moreover, according to Adel El Gammal, Secretary General of the European Energy Research Alliance (EERA), Europe accounts for 70% of Russian gas exports[30]. For Serbia, 81 % of its gas and 18 % of its oil and oil derivatives are imported from Russia[31]. At the end of May 2022, the Belgrade government obtained an agreement for the supply of Russian gas for a period of three years[32].

The struggles for influence around Serbian-Kosovar tensions are not only about security and defence, but also about energy resources and the protection of strategic areas, since Kosovo could also become a crossroads between the Adriatic coast (Albania and the port of Durres) and Eastern Europe, on the one hand, and the Aegean Sea (Northern Greece, the port of Thessaloniki) and the heart of Central Europe, on the other[33].

The consequences of these rivalries are still being felt, despite the war in Ukraine. Kosovo has increased its efforts to join the EU and NATO[34]while Serbia, while condemning the Russian invasion of Ukraine at the UN[35] and hosting Ukrainian refugees on its territory[36]The European Commission has refused to join the European Union in its sanctions against Russia[37].

All rights reserved by BRAUN

"We will not walk away and leave a vacuum to be filled by China, Russia, or Iran". These are the recent words of President Joe Biden at the summit GCC+3 (Gulf Cooperation Council + Egypt, Jordan and Iraq) in July 2022 in Jeddah, Saudi Arabia[1]. His speech comes in the context of the United States working to maintain its influence in the Middle East in the face of new rivals like the three countries mentioned above[2].

In recent years, contacts between the Arab countries of the Gulf, Iran, China and Russia have multiplied and consolidated[3]. Also, apart from military support to Syria and Iran, Russia and China have signed numerous arms contracts with countries in the region, such as Egypt and the GCC countries[4]. One can also think of the summits organised between the GCC and the USA's rivals, such as the recent visit of Russian Foreign Minister Lavrov to Riyadh in June 2022[5]. Finally, negotiations between the GCC and China for a free trade agreement are underway[6].

Despite the current tensions in the region, Saudi officials have repeatedly met with their Iranian counterparts with a view to de-escalating or even restoring diplomatic relations that have been severed since 2016[7]. Kuwait and Oman have repeatedly mediated disputes between Riyadh and Tehran[8]. After the end of the embargo in 2021, Qatar had offered to mediate between Tehran and the rest of the GCC countries[9]. For their part, the Emirates are currently preparing to send an ambassador to Tehran[10].

Energy interests (common gas fields, hydrocarbon supplies), economic interests (trade contracts, free trade agreements) and strategic interests (the Strait of Hormuz, the Gulf of Aden) explain these rapprochements[11]. However, the maintenance of American influence is mainly focused on security issues. The joint statement of the Jeddah Summiton " strengthening cooperation in the fields of defence, security and intelligence, as well as support for all diplomatic efforts to reduce regional tensions "[12]shows us this.

However, in the same statement, the participants expressed their "concern that the their commitment to joint cooperation to support global economic recovery efforts, address the economic impact of the pandemic and the war in Ukraine, ensure resilient supply chains and food and energy security, develop clean energy sources and technologies, and assist countries in need by meeting their humanitarian and relief needs "[13].

In addition, the participating leaders expressed their satisfaction with the creation of the Task Force 153 and the Task Force 59which " strengthen defence coordination between GCC member states and the US Central Command to better monitor maritime threats and improve naval defences using the latest technology and systems "[14]. The United States also welcomed the Arab Coordination Group (GAC) to provide a minimum of US$10 billion in response to regional and international food security challenges "[15].

On the occasion of Biden's visitSaudi Arabia and the United States have concluded 18 cooperation agreements in a wide variety of fields (space, finance, energy, health) as well as to connect the electricity networks of the Gulf countries to that of Iraq, which is very dependent on energy imported from Iran, a rival of both the Americans and the Saudis[16]. The 18 agreements were part of the Saudi Vision 2030 plan, and thirteen of them were signed with the Ministry of Investment, the Royal Commission for Jubail and Yanbuas well as various other private sector companies[17]. Saudi Arabia has signed agreements with several US companies such as Boeing Aerospace, Raytheon Defense Industries, Medtronic, Digital Diagnostics, IKVIA and IBM[18]. The Saudi Space Authority had signed the Artemis Agreements with NASA for joint exploration of the Moon and Mars[19]. The agreements also covered bilateral cooperation on technologies 5G and 6G[20]and supported Saudi projects aimed at making the Kingdom an innovation and technology hub for the Middle East and North Africa[21]. Finally, the agreements consisted of civil nuclear energy and uranium partnerships[22].

In the face of growing Russian, Chinese and Iranian influence in the Middle East, the maintenance of American influence can be sustained in the energy field, as well as in defence.[23]

All rights reserved by BRAUN

Despite the end of the Saudi embargo from 2017-2021, Doha-Tehran relations have been maintained and deepened. The same is true of Doha-Ankara relations[1].

In the case of Turkey, Ankara has expanded the capacity of its military base in Doha and has deployed over 5,000 troops there[2]. Several defence agreements have been signed, such as the June 2021 agreement on pilot training in Turkey[3]. In March 2022, at the Doha International Maritime Defence Exhibition (DIMDEX), the Qatari Ministry of Defence and four defence companies, including two Turkish companies, signed agreements and contracts for services and technology transfer[4].

For its part, Qatar has injected $15 billion into the Turkish economy, including at a time when the Turkish lira was significantly weakened (2018)[5]. In 2020, Turkey transferred 10 % of Istanbul Stock Exchange shares to the Qatar Investment Authority[6]. The latter bought for USD 1 billion the transfer of 42 % of the shares of one of Turkey's largest shopping centres, Istinye Park, located on Qatar Street in Istanbul[7]. In 2020 alone, total investment from Qatar to Turkey was $22 billion[8]. In 2021, this amount has increased to $ 33.2 billion, making Qatar the second largest investor in the country[9]. Since the creation of the Turkey-Qatar High Strategic Committee in 2014, 80 cooperation agreements were signed in many areas[10].

In addition, during the land, sea and air embargo, Doha received supplies from Turkish and Iranian planes and ships[11]. In June 2017 alone, in addition to a first ship loaded with 4,000 tons of food that sailed to Doha, Ankara had already sent 105 cargo planes with food aid to Qatar[12]. At the same time, Tehran was sending four cargo planes with food, and planned to send 100 tons of fruit and vegetables to Doha every day to prevent a food crisis in the country[13]. Finally, the flights of Qatar Airways, one of the world's largest airlines, were able to bypass the embargo, now transiting through Iran and Turkey[14].

Apart from logistical and humanitarian support, in many areas Qatar has formed a geopolitical alliance with Tehran and Ankara - mainly against Saudi Arabia[15]. In 2017, shortly after the Saudi embargo was put in place, the three countries signed an agreement on trade and transport[16]. The end of the embargo in 2021, decided at the Al Ula summit, did not put an end to the cooperation between Doha, Ankara and Tehran[17].

For example, in December 2021, Turkey and Qatar agreed to control and manage Kabul airport after the Taliban returned to power in Afghanistan[18]. The two countries also cooperate on Syria (against Al Assad), Palestine (aid and support to Hamas) and Libya (in favour of the Tripoli government)[19]. Turkey and Qatar are also known for their support of the Muslim Brotherhood, including during the Arab Spring (2010-2011)[20].

In the case of Iran-Qatar relations, there is the same continuity in bilateral relations as in the case of Turkey after the 2017-2021 embargo. One of the reasons is the shared possession of the world's largest gas field (North Dome/South Pars), which is essential for Doha[21]. Moreover, given that Qatar hosts the American base of Al Udeid and fears a possible attack on its territory, the country seeks to keep a maximum of diplomacy with Tehran[22]. Moreover, Doha had supported the Vienna agreements (JCPOA) in 2015[23] and works on de-escalation between Washington and Tehran as a mediator[24].

Recently, on 20-21 February 2022, Iranian President Raisi arrived in Doha for a state visit[25]. On his first visit to the Gulf, he signed 14 documents on agreements with Qatari officials, in the presence of the Emir[26]. Finally, he attended the 6th Gas Exporting Countries Forum (GECF) summit, which was held this year in the Qatari capital[27]. In addition to energy, the Iran-Qatar agreements are primarily focused on trade and the economy, as well as culture, education and infrastructure[28].

The current stakes of the Iran-Turkey-Qatar alliance are multiple, due to the diversity of the external relations of these three regional actors. First, Turkey is in NATO and, like Qatar, has American military bases in Izmir and Incirlik. However, Iran has military links with Russia and China, and supports the Syrian regime of Al Assad[29]. Even in the Ukrainian conflict, Iran and Russia have agreed on the delivery of arms (drones) as well as on gas and oil[30]. For its part, Turkey has delivered Bayraktar drones to Ukraine[31]. As for Qatar, it just "called on all parties to show restraint and resolve the crisis through diplomatic means".[32]. It can nevertheless become an alternative source of gas for Europe to Russian gas[33].

All rights reserved by BRAUN

On 13 March, Iran bombed Erbil, a large city in the north-east of Iraq inhabited mainly by the Kurdish population of the country. Tehran claimed responsibility for the strikes, which hit infrastructures that the Revolutionary Guards claim to be Israeli training complexes, but also strategic centres.

It is therefore a rivalry, an enmity that is ancient, deeply rooted in the consciousness and that echoes in our current situation. Since 2012, numerous air raids have been carried out by Israel against Syria. These tensions - whose link could easily be woven between the efforts of the United States and Tel Aviv to destabilise the Syrian regime of Bashar El-Assad, and the recent civil war suffered by Syrian society - have led to an increase in the number of Israeli interventions against Syria, aided by Iran.

On 7 March 2022 Israel bombed the suburbs of Damascus, killing two people. A small toll but a belligerent action that has no other purpose than the Hebrew determination to depose the Syrian leader. The reason for such a will is to be found in the particular relations that exist between Damascus and Tehran, both seats of countries with a Shiite majority, both opposed to the domination of Israel in the Middle East.

In response to the strikes near Damascus, which Tel Aviv says it carried out against the Iranian forces, Pasdaran, Iran bombed the city of Erbil in Iraqi Kurdistan, using the presence of US and Israeli military complexes as a pretext. Washington and the Hebrew state immediately denied the presence of bases belonging to them, pointing out that only a US Consulate is present in the city. New sanctions were imposed on Tehran.

However, as Iran is part of the Sino-Russian economic, military and energy alliance, the sanctions imposed on it have less and less effect, except on the European side. Indeed, European positions are unclear, with some countries such as France, Germany and Italy trying to maintain their market share in the country, but remaining timid, becoming uncertain commercial and diplomatic partners as soon as the United States calls them to order.

In the context of the Southern Russian war against Ukraine, in which the Donbass territories, i.e. the Russian-speaking regions of Donetsk and Luhansk, are the main issue, Iran has sided with Russia, waiting for China to take a stand. With the situation in the region taking precedence over all other crises of the moment, Israel took advantage of this window of opportunity to attack Iranian forces in Syria, attempting to further destabilise the El-Assad regime. The strikes launched from the territories near Iraq by Iran's revolutionary forces are a message to Israel, the United States and the rest of the West; Tehran remains ready to defend its interests, those of its allies, but above all to carry out its power project in the region, wanting to counter Tel Aviv's wishes.

All rights reserved by BRAUN

The Middle East is the scene of ancient rivalries that have taken a disturbing turn in recent decades, particularly since the founding of the State of Israel in 1948. These tensions are the consequence of ethical, religious and economic oppositions for the domination of the region by one or other of the powers involved. Indeed, on the one hand, the Arab countries of the Sunni Muslim faith, including the United Arab Emirates, Saudi Arabia, Qatar and Iraq - which have had quite conflicting relations for several centuries - and on the other, Turkey, also Sunni but of a different ethnicity from the Arabs, which is still opposed on many points. There is also Iran, a Muslim country, Shiite however, a sworn enemy of the Sunnis, allied to Lebanon, whose history is more affiliated with the Catholic Christians of the West, but governed by Shiites. Finally, at the centre of this unstable region is the young, Jewish Israeli state, which seems determined to reclaim the territories lost under Roman rule from 63 BC. The situation is increasingly critical, especially since several crises have erupted in the last century and in this one: the 1948 war, the 1956 Suez war, the 1967 Six-Day War, the 1967 War of Attrition, the 1973 Yom Kippur War, the 1982 First Lebanon War, and the 2006 Second Lebanon War. Today, one of the main areas of tension and concern is a small country on the Arabian Peninsula, Yemen.

Ravaged by a civil war since 2014, and for the second time since 1994[3]The conflict in Yemen is less publicised than in Iraq and Syria. The opposing parties are, on the one hand, the Houthis, who control a large part of the north of the country (including the capital Sana'a), and, on the other hand, the Yemeni governmental forces loyal to President Hadi in exile, who are mainly present in the south and east of Yemen[4]. Other belligerents are involved, such as the separatists of the Southern Transitional Council, who control Aden and its surroundings[5].

By analysing the causes and the course of this war, we notice that Yemen, despite being the poorest country in the Arabian Peninsula, is above all a strategic location[6]. Indeed, located along the Bab el Mandeb Strait, halfway between the Red Sea and the Gulf of Aden, it is a crossroads for maritime traffic from the Suez Canal (Egypt), the Gulf of Aqaba (Saudi Arabia and Israel) and the Indian Ocean[7]. It is located opposite Djibouti, home to French, American and Chinese military bases, and Somalia, which faces both piracy and Islamic radicalism[8].

The reason why this armed conflict is to be taken seriously, beyond the deaths it causes, is that it concerns the poorest region of the peninsula in the whole of the Arab world, but a strategic one. Indeed, lying at the Bab El-Mandeb Strait, halfway between the Red Sea and the Gulf of Aden, Yemen is an important maritime commercial crossroads for all goods coming from the Suez Canal, which is controlled by Egypt, from the Gulf of Aqaba, which is shared by Israel and Saudi Arabia, but also from the Indian Ocean.

Currently, two powers are vying for control of Yemen: Iran and Saudi Arabia[9]. The Houthis, Shiites like the majority of Iranians, are supported logistically and militarily by Tehran, and even have the support of the Lebanese Hezbollah, also supported by Iran[10]. This Iranian support represents a danger for Riyadh, which sees it as a manoeuvre of encirclement on the part of the Shiites, while tensions are already at their height between it and Tehran. Tensions present in other Arab countries, such as Bahrain, Iraq, Syria and Lebanon[11]. These problems are the pretext invoked by Saudi Arabia for its intervention in the Yemeni conflict since 2015, forming a coalition with several allied countries and increasing the number of raids on the areas controlled by the Houthis (Operations Decisive storm and Restoring hope)as well as through military support to Yemeni government forces[12]. The United Arab Emirates, an ally of Riyadh, supports the separatist forces in the South, also rivals of the Houthis[13].

The belligerents have received a great deal of foreign support in terms of armaments. In the case of Saudi Arabia, Riyadh has benefited from American and British support, notably for the training of its fighter pilots for aircraft manufactured by the United States or by Europe[14] - i.e. by France with the sales of Rafales. On the maritime front, Saudi Arabia also has European and American equipment[15]. 15] The Saudis are also seeking to replenish their missile supplies from the Americans[16]. Apart from the United States and Great Britain, France, Canada, Italy and Spain are also supplying arms to the Saudi-led coalition[17]. Belgium is also among the European countries that have authorised exports to Saudi Arabia[18]. The Saudi Kingdom, due to its involvement in the war in Yemen, is the world's largest importer of arms, with an increase of 61% in its supply between 2016 and 2020[19]. Riyadh has purchased nearly €1.4 billion worth of war materials from France, and French weapons have been found in Yemen[20]. 20] Saudi Arabia was Italy's third largest customer in the Middle East and North Africa last year. 21] The serial numbers on the recovered bomb fragments indicated that they were manufactured by the Italian company RWM, a subsidiary of the German Rheinmetall.

Gulf allies are supplied with modern weapons by Saudi Arabia and the United Arab Emirates[23]. In contrast, in Yemen, the weapons used by the Yemeni army are mainly of Russian design, while the Houthis benefit from Iranian support through the delivery of missiles and anti-tank weapons[24]. The Houthis have recently acquired a new type of Delta drone and a new model of land-based cruise missile[25]. The Houthis have several types of drones, some of them locally manufactured: the Samad-3, which can be equipped with 18kg of explosives, with a range of 1,500 kilometres, and a top speed of 250 km/hour; the Qasef-1 and Qasef-2, with a range of 150 km for a load of 30 kg of explosives; and finally, short-range reconnaissance drones such as the Rased (35 km), Hudhhud (30 km) and Raqib (15 km)[26].

Like Lebanon with Hezbollah, Iraq with its pro-Iranian militias, Syria with Al Assad, Yemen is one of the main fronts opposing Sunni Saudi Arabia and Shia Iran[27]. It is not only a civil war, but also a war of influence[28]. In addition, the Yemeni conflict has left the country economically drained[29]. In addition to the most serious humanitarian crisis in the world, people are often deprived of international aid, diverted by both the Houthis and the central government[30]. According to the director of the World Food Programme (WFP), in the capital of Sana'a alone, only 40 % of donations are reaching needy citizens, and only a third is receiving aid in the northern bastion of the rebel militia[31].

In recent months, the stalemate in which this conflict has fallen, the Houthi bombardment of Saudi and Emirati territories, see Saudi Arabia and Iran multiplying negotiations in order to normalise their relations, broken since 2016, and end the fighting[32]. Their results remain uncertain...

All rights reserved by BRAUN

Since 2013, after the Maïdan uprising in Kiev, the fate of the country has remained at a standstill. At the societal level, opinion is divided; on one side the nationalists and pro-Westerners, on the other the pro-Russians. Ukraine is facing a border crisis, following the annexation of Crimea by Russia and the conflict in the Donbass which has lasted since 2014, killing more than 14 000 people[1].

As a result of this internal and external turmoil, Ukraine is caught between two spheres of influence[2]. Indeed, from the point of view of external diplomacy, there is the fact that Russia wants to keep Ukraine in its zone of influence, while Western countries, both EU and NATO, seek to increase their presence in the country for strategic reasons - notably for access to the Black Sea[3]. Moreover, like Georgia, Ukraine has applied for membership of the European Union and NATO, which Russia strongly opposes.[4]The recent military moves are to be seen in this light.

Since 2014, EU-NATO-Ukraine contacts, partnerships, military exercises as well as bilateral relations with NATO member countries have increased and deepened.

For example, at the European level, an EU-Ukraine free trade agreement and a European visa waiver programme for Ukrainian nationals were signed in 2017[5]. In October 2021 the 23rd EU/Ukraine Summit took place in Kiev[6] and in December of the same year, an EU summit with the Eastern Partnership countries, including Ukraine, was held in Brussels in an attempt to de-escalate tensions with Russia[7].

Despite Russian opposition, NATO maintains its open door policy for Ukrainian membership of the alliance[8]. NATO's support takes the form of a range of assistance and aid measures, through 16 capacity-building programmes and trust funds[9]. Furthermore, at the NATO Summit in Warsaw in 2016, the NATO-Ukraine Platform for Combating Hybrid Warfare Practices was established[10]. Recently, the NATO Information and Communication Agency (NCIA) and Ukraine signed a new Memorandum of Understanding (MoU) on cooperation on technology projects[11].

Among the member states of both NATO and the EU, Poland and the Baltic states (Lithuania, Latvia, Estonia) are the most involved in partnerships and the deepening of common interests with Ukraine, including in defence. One example is the Lublin Triangle, created in July 2020, which brings together Poland, Lithuania and Ukraine[12]. To understand this greater proximity between these nations, one must remember their history; the former Republic of Poland-Lithuania, then the Grand Duchy of Poland, was always a major stake in the strategy of control of the region, either by the Poles, enemies of the Prussians but great allies of the French, or by the Russian Empire. It should also be remembered that Kiev was the first capital of the Rus until they moved to Moscow. Ukraine is a country whose independence is the result of agreements that are not old, signed in 1991. The country was first ruled by the Republic of Poland-Lithuania, then by the Russian Tsars, for whom the region was the granary until the fall of the Soviet Union in 1989.

However, Russia intends to maintain its positions, increasing the number of Russian troops along the Ukrainian border (situation before 24 February 2022), organising several military exercises with its allies, as recently with Belarus[13]. China recently declared its support for Russia in this crisis[14]. Some NATO member countries even express scepticism about Ukraine's entry into the alliance, particularly because of its economic, socio-political and energy interests with Russia (France, Italy, Germany and Hungary)[15]. The tensions created by the agreements on the exploitation and delivery of Russian gas to Europe should be understood here.

The numerous Russian-American meetings and visits to Europe by American officials, such as that of Secretary of State Blinken, concerned about the current situation in Ukraine, show that the country remains more than ever an East-West frontier, not only from a military and socio-economic point of view, but also from a geopolitical point of view[16]. Despite American and French efforts to avoid a Russian-Ukrainian escalation, the future of this "border" remains uncertain[17].

All rights reserved by BRAUN